Dan Ariely’s second TEDTalk premieres today — and so does the second, revised and expanded edition of his book Predictably Irrational. It’s full of new material, incuding Ariely’s thoughts on the irrationality of the economic collapse that happened since the book debuted in February 2008. Below, Ariely muses on the way the world has changed between then and now:

Before the financial crisis of 2008, it was rather difficult to convince people that we all might have irrational tendencies.

For example, after I gave a presentation at a conference, a fellow I’ll call Mr. Logic (a composite of many people I have debated with over the years) buttonholed me. “I enjoy hearing about all the different kinds of small-scale irrationalities that you demonstrate in your experiments,” he told me, handing me his card. “They’re quite interesting — great stories for cocktail parties.” He paused. “But you don’t understand how things work in the real world. Clearly, when it comes to making important decisions, all of these irrationalities disappear, because when it truly matters, people think carefully about their options before they act. And certainly when it comes to the stock market, where the decisions are critically important, all these irrationalities go away and rationality prevails.”

Given these kinds of responses, I was often left scratching my head, wondering why so many smart people are convinced that irrationality disappears when it comes to important decisions about money. Why do they assume that institutions, competition, and market mechanisms can inoculate us against mistakes? If competition was sufficient to overcome irrationality, wouldn’t that eliminate brawls in sporting competitions, or the irrational self-destructive behaviors of professional athletes? What is it about circumstances involving money and competition that might make people more rational? Do the defenders of rationality believe that we have different brain mechanisms for making small versus large decisions and yet another for dealing with the stock market? Or do they simply have a bone-deep belief that the invisible hand and the wisdom of the markets guarantee optimal behavior under all conditions?

Given these kinds of responses, I was often left scratching my head, wondering why so many smart people are convinced that irrationality disappears when it comes to important decisions about money. Why do they assume that institutions, competition, and market mechanisms can inoculate us against mistakes? If competition was sufficient to overcome irrationality, wouldn’t that eliminate brawls in sporting competitions, or the irrational self-destructive behaviors of professional athletes? What is it about circumstances involving money and competition that might make people more rational? Do the defenders of rationality believe that we have different brain mechanisms for making small versus large decisions and yet another for dealing with the stock market? Or do they simply have a bone-deep belief that the invisible hand and the wisdom of the markets guarantee optimal behavior under all conditions?

As a social scientist, I’m not sure which model describing human behavior in markets — rational economics, behavioral economics, or something else — is best, and I wish we could set up a series of experiments to figure this out. Unfortunately, since it is basically impossible to do any real experiments with the stock market, I’ve been left befuddled by the deep conviction in the rationality of the market. And I’ve wondered if we really want to build our financial institutions, our legal system, and our policies on such a foundation.

As I was asking myself these questions, something very big happened. Soon after Predictably Irrational was published, in early 2008, the financial world blew to smithereens, like something in a science fiction movie. Alan Greenspan, the formerly much-worshipped chairman of the Federal Reserve, told Congress in October 2008 that he was “shocked” (shocked!) that the markets did not work as anticipated, or automatically self-correct as they were supposed to. He said he made a mistake in assuming that the self-interest of organizations, specifically banks and others, was such that they were capable of protecting their own shareholders. For my part, I was shocked that Greenspan, one of the tireless advocates of deregulation and a true believer in letting market forces have their way, would publicly admit that his assumptions about the rationality of markets were wrong. A few months before this confession, I could never have imagined that Greenspan would utter such a statement. Aside from feeling vindicated, I also felt that Greenspan’s confession was an important step forward. After all, they say that the first step toward recovery is admitting you have a problem.

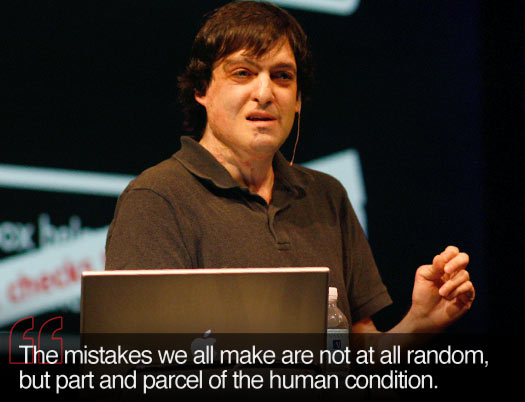

Still, the terrible loss of homes and jobs has been a very high price to pay for learning that we might not be as rational as Greenspan and other traditional economists had thought. What we’ve learned is that relying on standard economic theory alone as a guiding principle for building markets and institutions might, in fact, be dangerous. It has become tragically clear that the mistakes we all make are not at all random, but part and parcel of the human condition. Worse, our mistakes of judgment can aggregate in the market, sparking a scenario in which, much like an earthquake, no one has any idea what is happening. All of a sudden, it looked as if some people were beginning to understand that the study of small-scale mistakes was not just a source for amusing dinner-table anecdotes. I felt both exonerated and relieved.

While this is a very depressing time for the economy as a whole, and for all of us individually, the turnabout on Greenspan’s part has created new opportunities for behavioral economics, and for those willing to learn and alter the way they think and behave. From crisis comes opportunity, and perhaps this tragedy will cause us to finally accommodate new ideas, and — I hope — begin to rebuild.

Comments (8)